The best stay private forever

IPOs aren't the goal anymore. For the best founders, they're a distraction. Something you do when you have no other choice. The headaches are bigger, and the rewards don't justify the tradeoffs. The truth is, great companies don't need to go public anymore. So they don't.

Hit your quarter, stay out of the headlines, keep analysts happy. It's a system that punishes long-term thinking. Even the best operators—Musk, Bezos, Sundar—are stuck playing defense. Layer on regulatory complexity, ESG reporting, activist investors, and it's clear: if you don't have to IPO, you shouldn't.

Private Capital Has Changed the Game

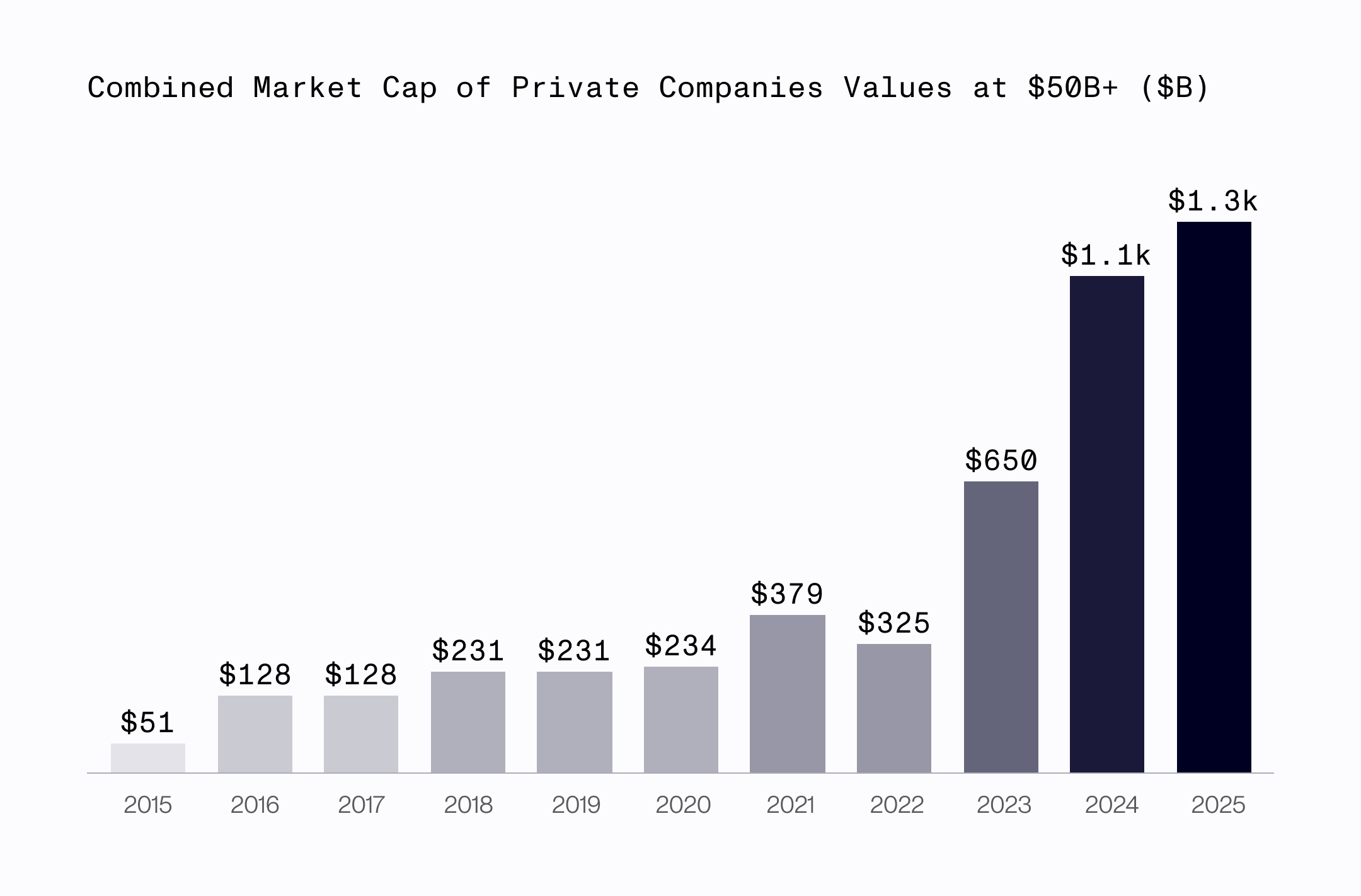

There was a time when public markets were the only way to raise meaningful growth capital. That era is over. Since the GFC, venture AUM has exploded from $300B to over $3T. What was once boutique is now institutionalized, and for good reason. Over the last 25 years, the number of publicly listed companies in the U.S. has dropped by more than 40% — from roughly 7,400 to around 4,300 — while private markets have ballooned to fill the gap (JPMorgan 2024 Annual Letter). The best growth stories don't need public markets anymore, and the capital that used to chase them there has followed them behind closed doors.

Today, late-stage private rounds routinely hit $500M+. OpenAI raised $6.6B, Stripe raised $6.5B, Databricks $10B — all without listing a single share. These used to be public-market events. Now they're happening in cap tables, led by crossovers, sovereigns, and pension funds who need exposure to the best growth stories to keep up with their obligations.

Just like growth capital, liquidity for early team and investors used to be a big reason to go public. That's not true anymore either. Secondaries have exploded into a real liquidity path for anyone who needs it. SpaceX, Stripe, OpenAI, Databricks proved it many times over: for the companies where demand exceeds primary supply, secondaries clear at or above the last round price. And the mechanics have matured. Early shareholders with even fractional positions can find buyers willing to absorb their stake at market price, recycle capital into the next cycle, and keep compounding — no IPO required. The exit isn't the event anymore. Liquidity is a continuous process.

Permanent Capital Wins

Thrive, Coatue, Sequoia, Tiger—they're not venture funds in the traditional sense. They're permanent capital platforms. They don't need to exit. They're not playing for DPI. They're building Blackstone-like positions in the best private companies and holding for as long as they want.

There's no more room at that table. The franchise window is closed. Just like there won't be another Vanguard or Fidelity, there won't be another Sequoia. Competing with these platforms at growth is a losing game. If you're not already in the round, you're not getting in.

So What Now?

For retail investors? The door's mostly shut. The Mag 7 carried the S&P for the last decade. Once that's done, there's not another class of mega-cap IPOs waiting in the wings. Most of the upside has already been captured in private.

But for family offices and UHNW investors, the strategy is clear: barbell it. (1) Anchor on late-stage private positions with public-like multiples — the permanent capital platforms will keep manufacturing these, and secondary markets make them accessible to investors who can't commit a quarter billion to a flagship fund. (2) Get in early where possible, through networks of operators and emerging managers writing first checks before signals exist — this is where the real multiple expansion lives, and it's increasingly where the best founders start. (3) Use secondaries as a way in, not just a way out — early positions in breakout companies can be partially monetized to fund the next cycle, creating a self-sustaining loop that doesn't depend on an IPO that isn't coming.

Liquidity is no longer a finish line—it's a tool. For early-stage investors, secondaries aren't an emergency exit. They're capital recycling. They're what lets you keep playing, keep backing the next one, and compound winners before the market ever gets a taste.

The Old Playbook Is Over

Venture used to be: fund managers, wait for IPOs, return capital, rinse, repeat. That model doesn't work anymore. The best companies aren't exiting, and capital sitting on the sidelines is just getting diluted.

We're in a new era. The entry points are shifting. The check sizes are shrinking. The window is smaller, faster, and earlier than it's ever been. The ones who adapt will own the next decade of returns. Everyone else will just keep waiting.